꼭 알아야 하는 내용

PPO vs HMO 이해하기: 미국 건강보험의 기본

PPO (Preferred Provider Organization) & HMO (Health Maintenance Organization)

In-Network & Out-of-Network

기준 | PPO | HMO |

네트워크 유연성 | In-network 및 out-of-network 사용 가능, 그러나 비용은 달라짐 | 제한적 네트워크, 주로 in-network 안에서만 사용 가능 |

주치의 (PCP)

| 주치의 선택 필수는 아님 | 주치의 지정 꼭 필요 |

전문의 의뢰

| 의뢰서 없이 전문의 방문 가능 | 주치의 의뢰서 (Referral) 가 꼭 필요 |

서비스 접근성 | 높은 자유도, 다양한 제공자 선택 가능 | 제한적, 주치의를 통한 접근 필요 |

미국 건강보험 사용에 꼭 이해해야할 용어 7가지

보험료(Premium): 보험사에 지불하는 월간 또는 연간 요금입니다.

최대 자기 부담금(Maximum out-of-pocket expense): 보험 고객이 지불해야 하는 최대 금액입니다. 이 금액을 초과할 경우, 보험사가 추가적인 의료 비용을 전액 부담합니다.

자기 부담금(Deductible): 보험료를 지불한 후, 보험사가 보장하는 의료 서비스를 받을 때 고객이 지불해야 하는 금액입니다.

공동보험 (Coinsurance): 의료 서비스에 대한 비용의 일부를 보험회사와 환자가 나누어 부담하는 것입니다. 일반적으로 보험회사가 일정 비율을 지불하고, 환자가 나머지 비용을 부담합니다. 예를들어 환자는 의료 서비스 비용의 30-50%를 부담합니다. 나머지 금액을 보험사가 부담합니다.

공동부담금 (Copayment): 환자가 진료와 관련된 비용의 일부를 지불하는 것입니다. 즉, 보험회사와 환자가 비용을 나누어 부담하는 것입니다. 일반적으로 의료 서비스를 받을 때 즉시 지불해야 합니다.

공동 보험(Family coverage): 두 명 이상의 가족 구성원이 한 보험 계약에 가입하는 것을 의미합니다.

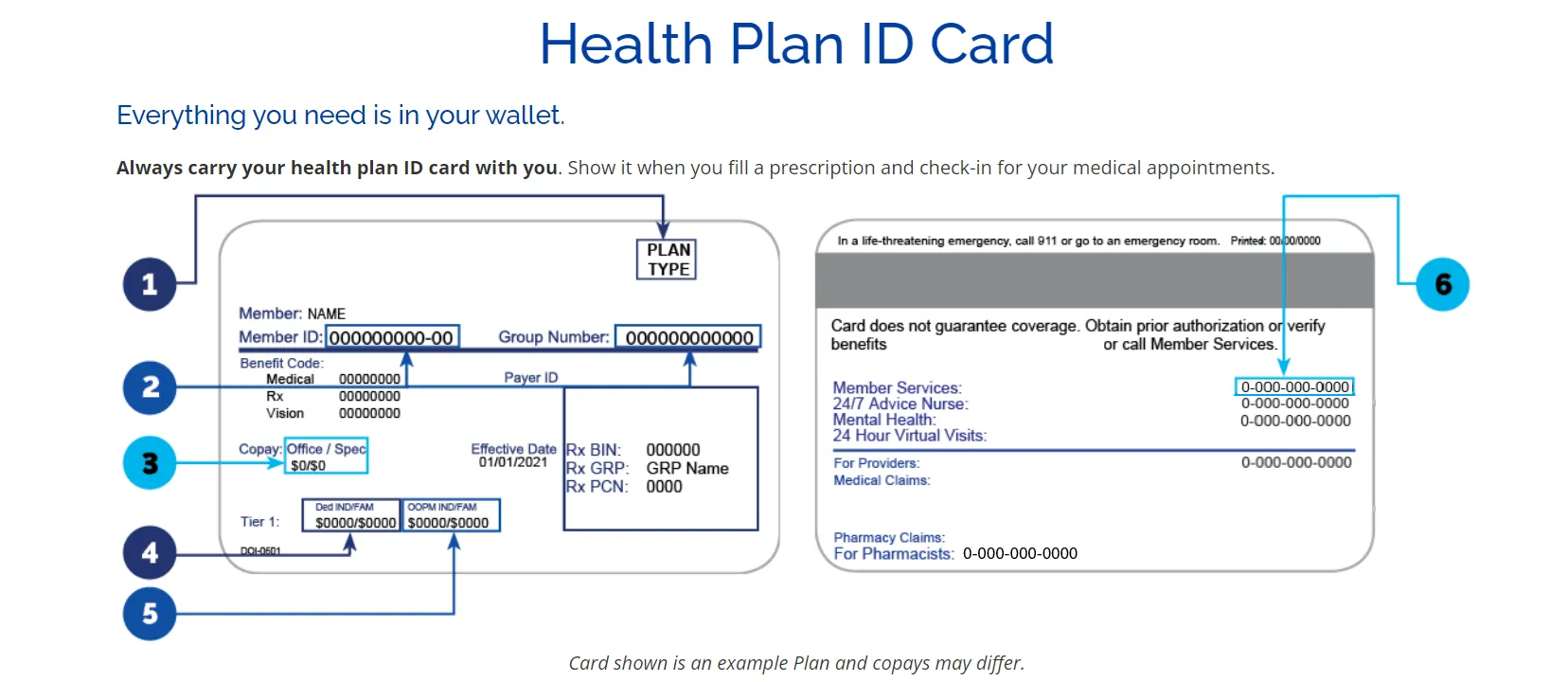

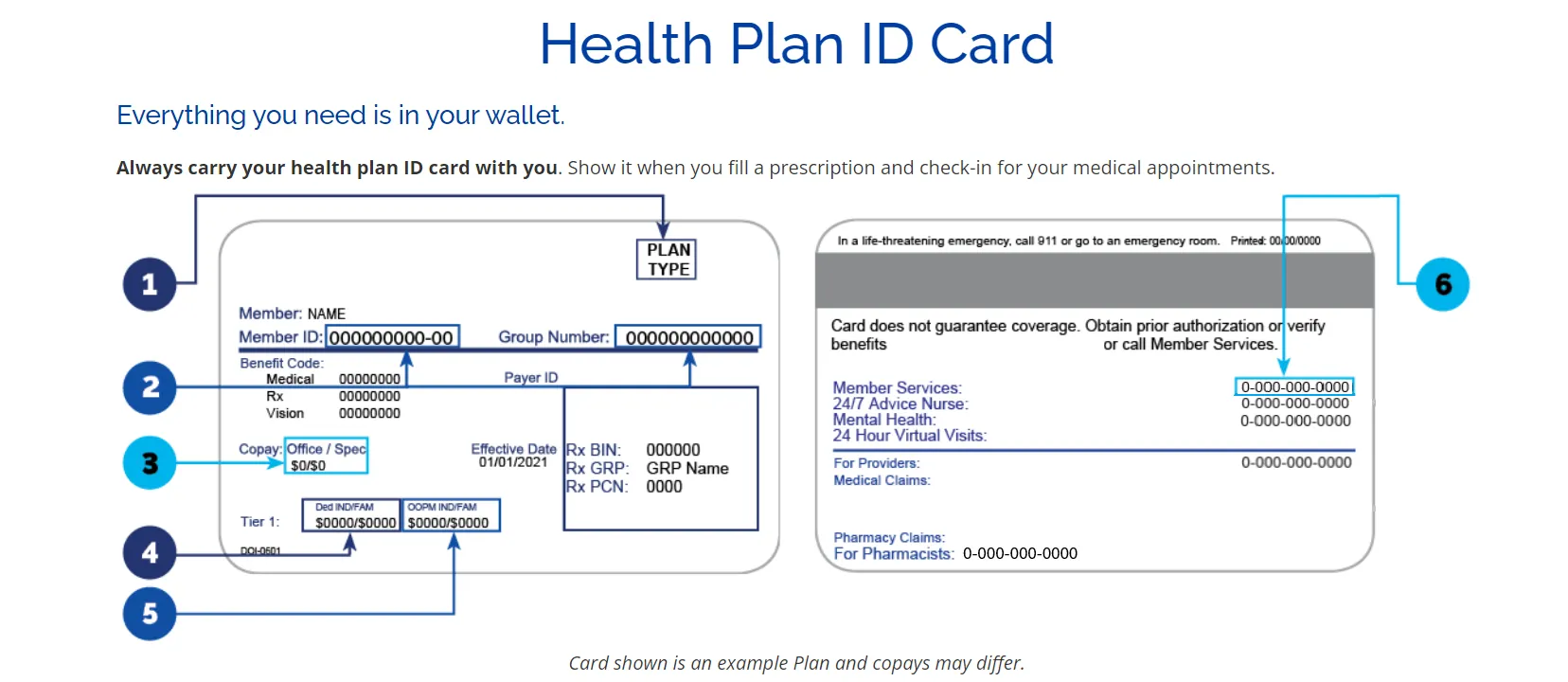

ID Card: 건강보험 ID 카드에는 보험 가입자 이름, 보험 가입자 ID 번호, 보험 가입자 그룹 번호, 보험 플랜 이름 또는 번호, 네트워크 정보가 포함될 수 있습니다.

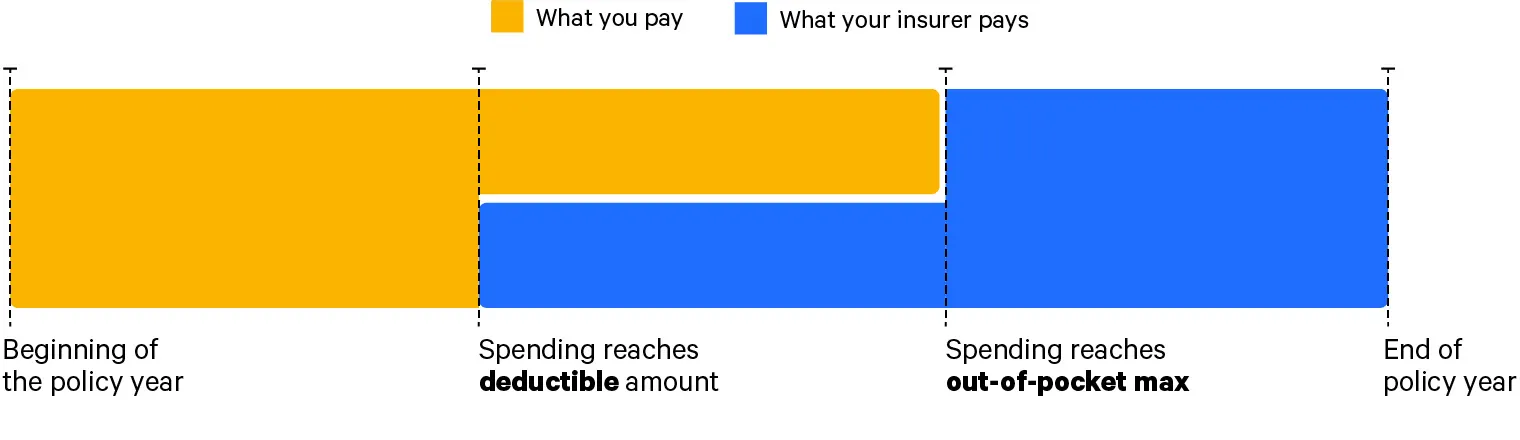

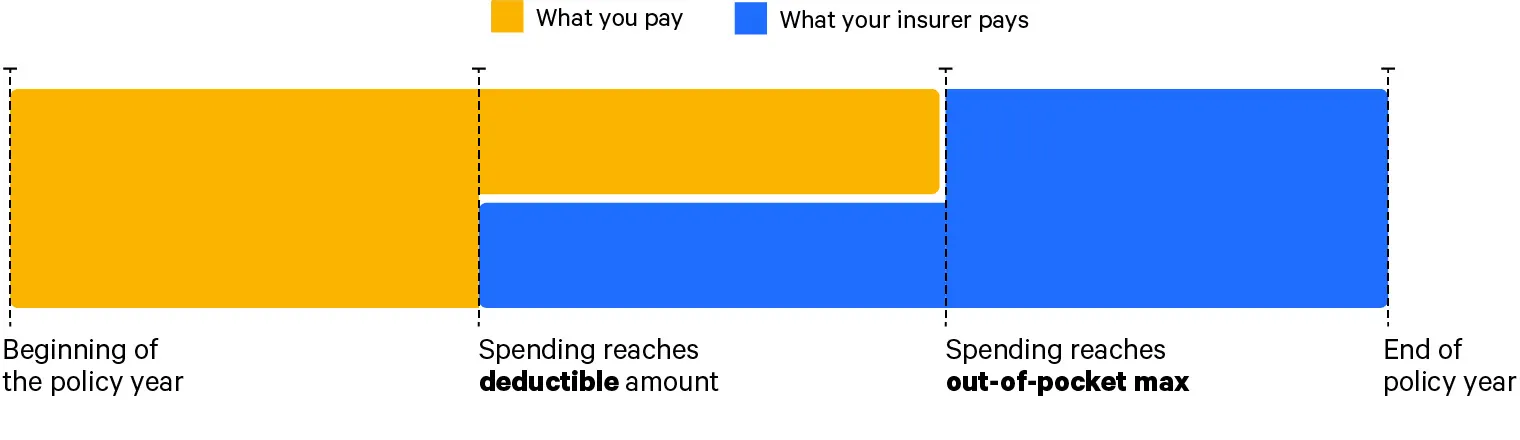

Deductible vs. Out-of-Pocket Max

ID Card (보험카드)

1.

Type of Plan

2.

Member ID and Group Number

3.

Copay

4.

Plan deductible (in network and out-of-network)

5.

Out-of-pocket maximums (in network and out-of-network)

6.

Member Services

Understanding Health Insurance

Useful Information to Know

In-Network vs Out-of-Network

Understanding PPO vs HMO: The Basics of U.S. Health Insurance

PPO (Preferred Provider Organization) & HMO (Health Maintenance Organization)

Criteria | PPO | HMO |

Network Flexibility | In-network and out-of-network usage is possible, but costs may vary. | Limited network, primarily only usable within the in-network. |

Primary Care Physician (PCP)

| Choosing a primary care physician is not required. | Designating a primary care physician is required. |

Specialist Referral

| Specialist visits are possible without a referral. | A referral from a primary care physician is required. |

Service Accessibility | High flexibility, with a wide choice of providers available. | Limited access, requiring access through a primary care physician. |

7 Essential Terms to Understand for Using U.S. Health Insurance

Premium: The monthly or annual fee paid to the insurance company.

Maximum out-of-pocket expense: The maximum amount that an insurance customer has to pay. Once this amount is exceeded, the insurance company covers all additional medical costs.

Deductible: The amount that the customer must pay when receiving medical services covered by the insurance, after paying the premium.

Coinsurance: This is the portion of medical service costs shared between the insurance company and the patient. Typically, the insurance company pays a certain percentage, and the patient is responsible for the remaining costs. For example, the patient might pay 30-50% of the medical service costs, with the insurance company covering the rest.

Copayment: This is the portion of the cost that the patient pays for medical services. In other words, the insurance company and the patient share the cost. It usually needs to be paid immediately when receiving medical services.

Family coverage: This refers to when two or more family members are enrolled under a single insurance contract.

ID Card: A health insurance ID card may include the subscriber's name, subscriber ID number, group number, plan name or number, and network information.

Deductible vs. Out-of-Pocket Max

Insurance ID Card

1.

Type of Plan

2.

Member ID and Group Number

3.

Copay

4.

Plan deductible (in network and out-of-network)

5.

Out-of-pocket maximums (in network and out-of-network)

6.

Member Services